Real Estate Wholesaling Contracts Explained: The Complete Guide for 2026

You've found a great deal under market value, but you don't have the cash or credit to buy it yourself. That's where a real estate wholesaling contract comes in — it's the legal tool that lets you lock up a property and sell your position to another buyer for a fee. Get this contract wrong, and you could lose the deal or even face a lawsuit. Get it right, and you can scale your wholesaling business without ever needing a bank loan.

Key Takeaways

- A real estate wholesaling contract is a purchase agreement with an assignment clause that lets you transfer your rights to a third party.

- The two main contract types are an "assignment of contract" and a "double close" — each has different legal and tax implications.

- Every wholesaling contract must include key clauses: assignment rights, inspection period, and clear purchase price terms.

- State laws vary widely — some require a real estate license to wholesale, others ban assignments altogether.

- As of 2026, the median US home price is $403,200 and mortgage rates are 6.49%, making creative financing like wholesaling more attractive than ever.

What Is a Real Estate Wholesaling Contract?

A real estate wholesaling contract is a legally binding purchase agreement between a wholesaler (you) and a property seller, which includes a clause allowing the wholesaler to assign their rights under the contract to another buyer before closing. In simple terms: you sign a contract to buy a property, but instead of actually buying it, you find an end buyer who pays you a fee to take over your spot.

The wholesaler never takes legal title to the property. Instead, they control the contract and sell that control for a profit — typically called an "assignment fee."

How This Differs from a Traditional Purchase Agreement

A standard purchase agreement is a two-party contract: buyer and seller. The buyer is expected to perform — meaning bring the cash or financing to closing and take title. A wholesaling contract is a three-party transaction in disguise. You (the wholesaler) are the middleman. You sign as the buyer, but your true intention is never to own the property. You intend to find a third party (the end buyer) who will step into your shoes before closing.

This distinction is critical because it changes how you negotiate, what clauses you need, and how you disclose your role. If you sign a standard purchase agreement without an assignment clause, you are legally obligated to buy the property yourself. If you can't, the seller can sue you for breach of contract or keep your earnest money.

Real-World Example: The $30,000 Assignment Fee

Imagine you find a three-bedroom home in a suburban neighborhood. The seller, an elderly couple moving into assisted living, needs to sell quickly. The home is dated — popcorn ceilings, old carpet, a roof that needs replacing. You estimate the after-repair value (ARV) at $250,000. You negotiate a purchase price of $200,000, knowing that a flipper can put $30,000 into repairs and still make a profit.

You sign a wholesaling contract with a 21-day inspection period. During those 21 days, you market the contract to your network of investors. You find a flipper who agrees to pay $230,000 for the contract. At closing, the flipper brings the cash, the seller gets $200,000, and you collect a $30,000 assignment fee. You never owned the house, never needed a loan, and never paid closing costs beyond a small fee.

How Do Real Estate Wholesaling Contracts Work?

Wholesaling works because of a simple legal mechanism: assignment. Most purchase agreements are assignable unless they specifically say otherwise. When you assign a contract, you transfer all your rights and obligations as the buyer to someone else — the end buyer.

Here's the step-by-step process:

- Find a motivated seller — Someone who needs to sell quickly, often because of financial distress, divorce, or a dated property.

- Negotiate a purchase price — You agree on a price that's well below market value, say $200,000 for a house worth $250,000.

- Sign a purchase agreement — This is your wholesaling contract. It must include an assignment clause or be silent on assignment (which generally allows it).

- Find an end buyer — You market the contract to other investors, flippers, or landlords.

- Assign the contract — You and the end buyer sign an assignment agreement. The end buyer pays you an assignment fee (e.g., $30,000) and steps into your shoes.

- Close — The end buyer brings the cash or financing, and the seller gets their money. You collect your fee at closing.

The Assignment Fee

Your profit is the difference between the contract price you negotiated with the seller and the price the end buyer pays you. In the example above, if you contracted at $200,000 and assigned to an end buyer for $230,000, your assignment fee is $30,000.

Step-by-Step: How to Execute an Assignment

Let's walk through the mechanics of step 5 in detail. Once you have an end buyer, you need to formalize the assignment. Here's the exact process:

- Draft an Assignment Agreement — This is a separate document from the original purchase agreement. It states that you (the assignor) are transferring all your rights and obligations under the original contract to the end buyer (the assignee). Include the property address, the original contract date, and the assignment fee amount.

- Get the End Buyer's Signature — The end buyer signs the assignment agreement, agreeing to step into your shoes. They also agree to pay you the assignment fee, typically at closing.

- Notify the Seller — In most states, you are not required to get the seller's permission to assign (if the contract allows it), but it's good practice to notify them. Some wholesalers include a "Notice of Assignment" letter that is sent to the seller and the title company.

- Coordinate with the Title Company — The title company will handle the closing. They need a copy of the assignment agreement to know who the actual buyer is and how to disburse the assignment fee. Some title companies require the assignment fee to be paid directly by the end buyer, while others will deduct it from the proceeds and pay you.

- Close — The end buyer brings the funds, the seller signs the deed, and the title company disburses the money. You receive your assignment fee, minus any agreed-upon closing costs.

What Happens If You Can't Find an End Buyer?

This is the risk every wholesaler faces. If your inspection period expires and you haven't found a buyer, you have two options:

- Exercise your right to cancel — If your contract has a due diligence or inspection period, you can simply cancel and get your earnest money back. This is why a long inspection period is critical.

- Extend the deadline — You can negotiate with the seller for more time. This might require additional earnest money or a price reduction.

- Buy the property yourself — If you have the funds or can get financing, you can close on the property and then resell it later. This is essentially a double close (discussed below).

What Are the Two Main Types of Wholesaling Contracts?

There are two primary ways to structure a wholesale deal: assignment of contract and double close. Each has pros and cons.

Assignment of Contract

This is the most common method. You sign a purchase agreement with the seller and then assign that agreement to an end buyer. The end buyer buys directly from the seller, and you get paid an assignment fee at closing.

Pros:

- Simple and low cost — usually just one closing.

- No need to come up with purchase funds.

- Less paperwork.

Cons:

- Some title companies won't handle assignments.

- The seller sees your assignment fee (it's disclosed on the HUD-1).

- Some states restrict or ban assignments.

Double Close (aka Simultaneous Close)

In a double close, you actually buy the property from the seller (using transactional funding or a hard money lender) and then immediately resell it to the end buyer on the same day. Two closings happen back-to-back.

Pros:

- Your profit is hidden from the seller (it's a wholesale markup).

- More title companies will work with you.

- Can be structured to avoid assignment restrictions.

Cons:

- You need transactional funding (short-term money) to buy the property.

- Two sets of closing costs eat into your profit.

- More paperwork and legal complexity.

How to Execute a Double Close

A double close requires more coordination but offers more privacy. Here's how it works:

- Secure Transactional Funding — You need a lender who will provide short-term funds (often for 1–3 days) to buy the property. Transactional funding is typically 100% of the purchase price, plus closing costs. The interest rate is high (often 2–3 points), but since you only hold the money for a few hours, the cost is manageable.

- Close with the Seller (First Close) — You use the transactional funding to buy the property from the seller. You take legal title for a few minutes or hours.

- Close with the End Buyer (Second Close) — Immediately after the first close, you sell the property to the end buyer at a higher price. The end buyer's funds pay off the transactional funding lender and give you your profit.

- Disburse the Profit — Your profit is the difference between the two sale prices, minus closing costs for both transactions.

Comparison Table: Assignment vs. Double Close

| Feature | Assignment of Contract | Double Close |

|---|---|---|

| Funding needed | None | Transactional funding required |

| Closings | One | Two (simultaneous) |

| Profit disclosed to seller | Yes | No |

| Title company acceptance | Some reject | Most accept |

| Legal risk in restrictive states | Higher | Lower |

| Typical closing costs | Lower | Higher (two sets) |

Which Method Should You Choose?

- Choose assignment if you're in a state that allows it, you have a title company that handles assignments, and you want to keep costs low.

- Choose double close if you're in a restrictive state (like Florida or Georgia), you want to hide your profit from the seller, or your title company refuses assignments.

What Clauses Must Every Wholesaling Contract Include?

A solid wholesaling contract protects you and makes the deal easy to assign. Here are the non-negotiable clauses:

1. Assignment Clause

This clause explicitly states that you can assign the contract to another party. Ideally, it says: "Buyer has the right to assign this contract to any person or entity without the consent of the Seller." If the contract is silent, assignment is generally allowed, but an explicit clause is safer.

2. Inspection Period (Due Diligence Period)

You need time to find an end buyer. A typical inspection period is 7–21 days. During this time, you can back out for any reason and get your earnest money back. This is your "escape hatch."

3. Clear Purchase Price and Terms

The contract must state the exact purchase price, earnest money amount, closing date, and any contingencies (like financing or inspection). Keep it simple — avoid complex terms that scare off end buyers.

4. No Financing Contingency (or Assignable Financing)

If you include a financing contingency, the end buyer might not be able to assume it. Better to have no financing contingency or make it clear that the contract can be assigned to a cash buyer.

5. Time is of the Essence

This clause ensures that all deadlines are strict. If you miss a deadline, you could lose the deal. It also gives the end buyer confidence that the timeline is firm.

6. Entire Agreement Clause

This says the written contract is the entire agreement — no oral promises. It prevents the seller from later claiming you agreed to something else.

How to Draft Each Clause

Let's go deeper into the language you should use for each clause.

Assignment Clause Example:

"Buyer shall have the right to assign this Agreement, in whole or in part, to any person or entity at any time, with or without the consent of Seller. Upon assignment, Buyer shall be relieved of all obligations under this Agreement, and the assignee shall assume all rights and obligations of Buyer. Buyer shall not be required to disclose the identity of the assignee or the terms of the assignment to Seller."

Inspection Period Clause Example:

"Buyer shall have a period of 21 days from the date of this Agreement (the 'Inspection Period') to conduct any and all inspections, investigations, and due diligence Buyer deems necessary. Buyer may terminate this Agreement for any reason or no reason during the Inspection Period by providing written notice to Seller. Upon termination, Buyer's earnest money shall be returned in full."

No Financing Contingency Clause Example:

"This Agreement is not contingent upon Buyer obtaining financing. Buyer acknowledges that this is a cash transaction and that Buyer's obligations hereunder are absolute and unconditional."

Time is of the Essence Clause Example:

"Time is of the essence with respect to all deadlines and time periods set forth in this Agreement. If Buyer fails to perform any obligation within the time specified, Seller may terminate this Agreement and retain Buyer's earnest money as liquidated damages."

Entire Agreement Clause Example:

"This Agreement constitutes the entire agreement between the parties and supersedes all prior negotiations, representations, and agreements, whether oral or written. No modification of this Agreement shall be effective unless in writing and signed by both parties."

Why Are State Laws Critical for Wholesaling Contracts?

Wholesaling is legal in most states, but some have specific laws that can trip you up. A few states require a real estate license to wholesale, while others ban assignments altogether.

States Where Wholesaling Is Restricted

- Florida — A 2021 law requires wholesalers to disclose their license status and prohibits assigning contracts on residential properties with more than one unit unless you're a licensed agent.

- Georgia — A 2022 law requires wholesalers to have a written agreement with the seller and prohibits marketing a property without a contract.

- New York — Courts have ruled that wholesaling without a license can be considered unlicensed real estate brokerage.

- California — Wholesaling is legal, but you must disclose your assignment fee to the seller.

How to Check Your State's Laws

Before you start wholesaling, take these steps:

- Visit your state's real estate commission website — Look for guidance on wholesaling, assignment of contracts, and license requirements.

- Consult a local real estate attorney — Spend $200–$500 for a one-hour consultation. Ask specifically: "Is wholesaling without a license legal in this state? What disclosures are required?"

- Join a local real estate investor association (REIA) — Members often share their experiences and can recommend attorneys who specialize in wholesaling.

- Read recent court cases — Search for "wholesaling real estate [your state] lawsuit" to see if there have been any recent rulings that affect your business.

What to Do If Your State Restricts Wholesaling

If you're in a state like Florida or Georgia, you have options:

- Get a real estate license — This is the safest route. You can wholesale legally and also earn commissions on the deals.

- Use a double close — As discussed above, a double close can bypass assignment restrictions because you actually take title (even if only for a moment).

- Partner with a licensed agent — Find a licensed real estate agent who is willing to co-sign the contract or act as the buyer of record. You split the profit.

- Focus on commercial properties — Some state laws only apply to residential properties. Commercial wholesaling may be less regulated.

How to Write a Wholesaling Contract (Step-by-Step)

You don't need to reinvent the wheel. Most wholesalers use a standard state-specific purchase agreement (like the Texas TREC form or California CAR form) and add an assignment addendum. Here's how to do it:

- Get a template — Use a standard purchase agreement from your state's real estate board or a wholesaling-specific template from a reputable source.

- Fill in the basics — Property address, purchase price, earnest money amount, closing date (typically 30–60 days out).

- Add the assignment clause — Either include it in the contract or use a separate "Assignment of Real Estate Purchase Contract" addendum.

- Set the inspection period — Make it long enough to find a buyer (14–21 days is common).

- Sign with the seller — Both parties sign. You give the seller a small earnest money deposit (often $100–$500).

- Market the contract — Use your network, social media, or a platform like PropStream to find end buyers.

- Assign the contract — Once you have a buyer, sign an assignment agreement. The end buyer pays you the assignment fee.

Sample Assignment Clause

"Buyer has the right to assign this Agreement, in whole or in part, to any person or entity without the consent of Seller. Upon assignment, Buyer shall be relieved of all obligations under this Agreement, and the assignee shall assume all rights and obligations of Buyer."

Where to Get Reliable Templates

- State Real Estate Board Forms — Many states (like Texas, California, and Florida) have standardized forms that are legally compliant. You can often purchase them from the state association of Realtors.

- Wholesaling-Specific Providers — Companies like Rezzie, DealMachine, and Wholesale Real Estate Network offer templates designed specifically for wholesalers.

- Real Estate Attorney — The safest option. An attorney can draft a contract that complies with your state's laws and includes all necessary clauses.

Common Mistakes When Filling Out the Contract

- Incorrect property address — Double-check the legal description and parcel number.

- Missing earnest money details — Specify the amount, who holds it, and under what conditions it is refundable.

- Vague closing date — Use a specific date (e.g., "on or before August 15, 2026") rather than "within 30 days."

- No signature lines for assignment — Make sure the assignment addendum has signature lines for you, the end buyer, and (if required) the seller.

What Are Common Mistakes in Wholesaling Contracts?

Even experienced wholesalers make errors. Here are the most common pitfalls:

1. No Assignment Clause

If your contract doesn't explicitly allow assignment, the seller could refuse to let you assign it. Always include an assignment clause.

2. Too Short an Inspection Period

If you only have 5 days to find a buyer, you're under pressure. Give yourself at least 14 days.

3. Not Disclosing Your Role

In some states, failing to disclose that you're assigning the contract can be considered fraud. Always be transparent with the seller.

4. Using the Wrong Contract Form

A generic online contract might not comply with your state's laws. Use a state-approved form or have an attorney review it.

5. Ignoring the Earnest Money

If you don't perform, the seller keeps your earnest money. Make sure the amount is small enough that you can afford to lose it.

How to Avoid Each Mistake

Mistake 1: No Assignment Clause

- Fix: Always include an explicit assignment clause. If you're using a standard purchase agreement, add an "Assignment Addendum" that states your right to assign.

Mistake 2: Too Short an Inspection Period

- Fix: Negotiate for at least 14 days. If the seller pushes back, explain that you need time for inspections and financing (even if you plan to assign). A 21-day period is ideal.

Mistake 3: Not Disclosing Your Role

- Fix: Be upfront with the seller. Say something like: "I'm an investor. I may assign this contract to another buyer before closing. You'll still get your full purchase price." In states like California, you must disclose the assignment fee in writing.

Mistake 4: Using the Wrong Contract Form

- Fix: Use a form that is approved by your state's real estate commission. If you're unsure, pay an attorney $200 to review your template.

Mistake 5: Ignoring the Earnest Money

- Fix: Keep your earnest money deposit low — $100 to $500 is typical. Never put down more than you can afford to lose. If the deal falls through, you walk away without a significant loss.

How Does the Current Market Affect Wholesaling Contracts?

As of mid-2026, the real estate market presents both challenges and opportunities for wholesalers.

Mortgage Rates at 6.49%

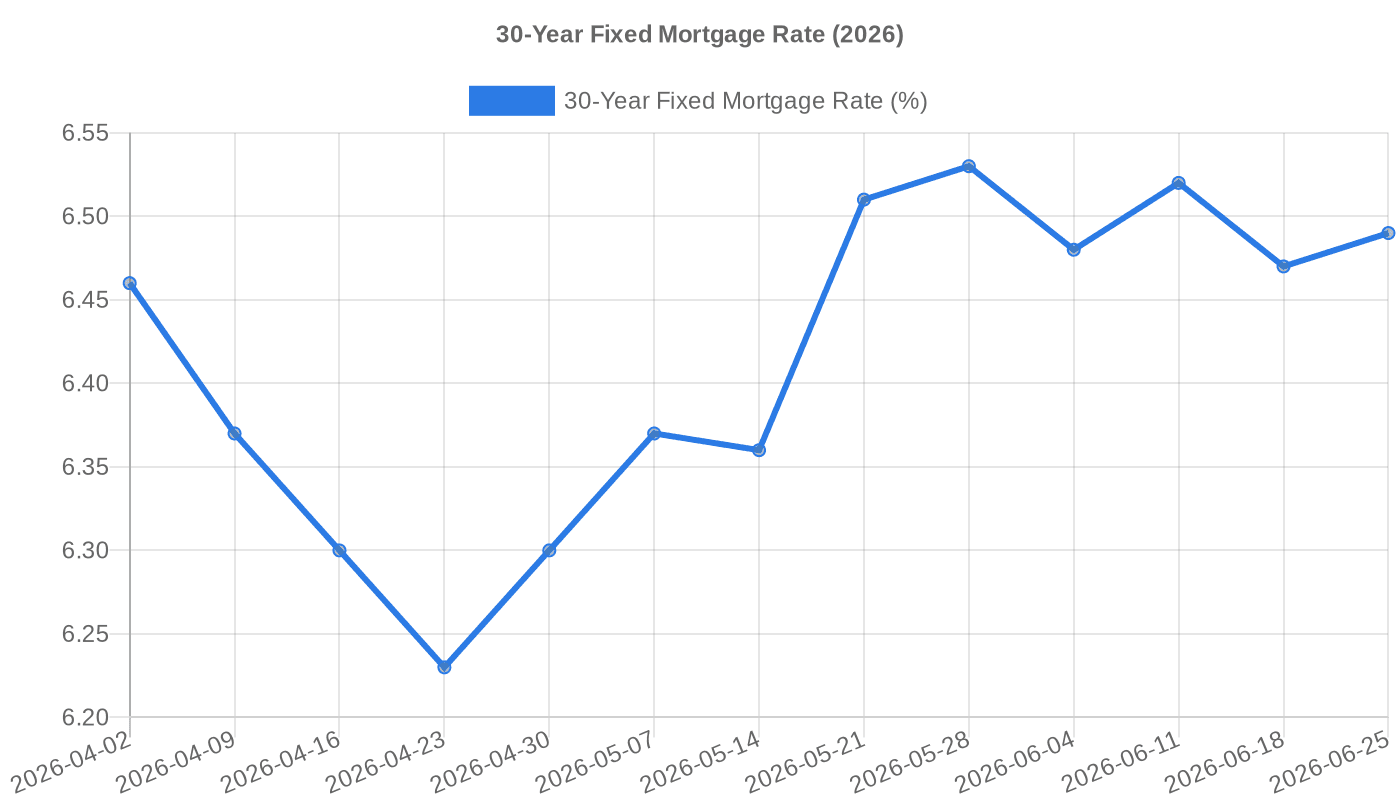

The 30-year fixed mortgage rate is 6.49% as of June 25, 2026. While not as low as 2021, rates have stabilized after a volatile period. Higher rates mean fewer traditional buyers can afford to purchase, which increases demand for creative financing like wholesaling.

Median Home Price at $403,200

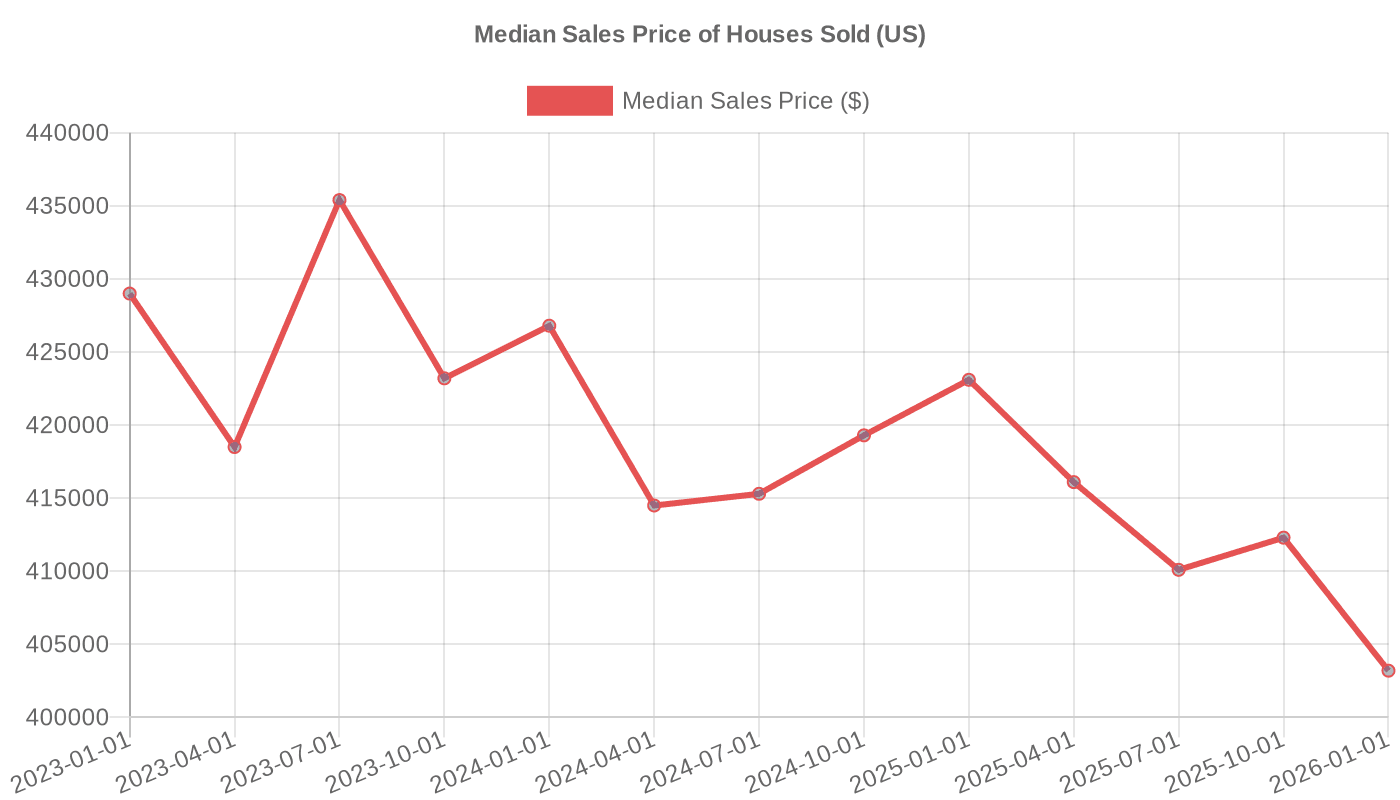

The median sales price of houses sold in the US was $403,200 as of January 1, 2026. Prices have softened slightly from the peak of $435,400 in mid-2023, but they remain elevated. This creates a wide gap between what motivated sellers need and what the market will bear — perfect for wholesalers.

Days on Market at 52 Days

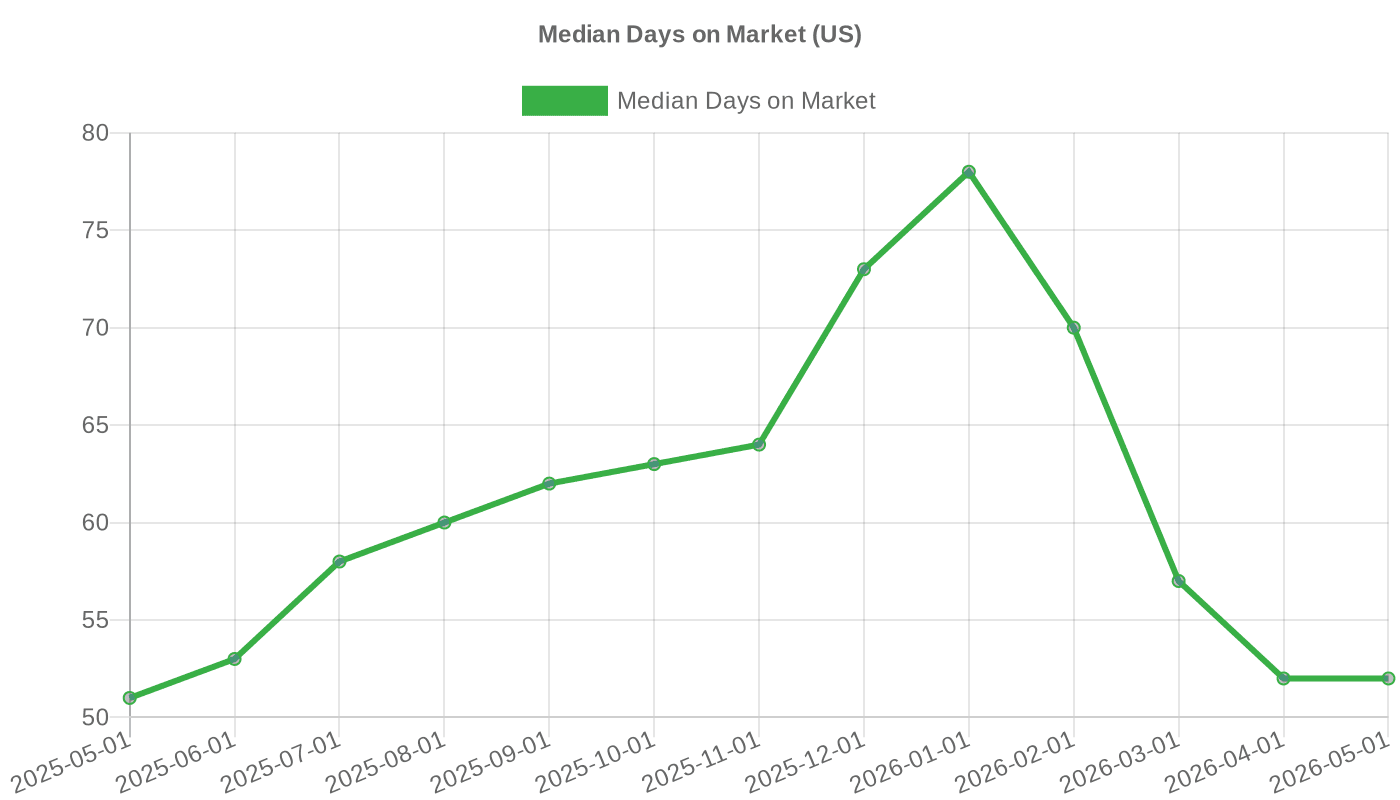

As of May 2026, the median days on market is 52 days, down from 78 days in January 2026. This means properties are selling faster than earlier in the year, but still slower than the red-hot market of 2021–2022. Slower markets give wholesalers more time to find deals and assign contracts.

How to Adapt Your Wholesaling Strategy to the Current Market

- Focus on motivated sellers — With higher rates, sellers who need to move quickly (due to divorce, job relocation, or foreclosure) are more common. Target these sellers with direct mail, bandit signs, and cold calling.

- Price your deals conservatively — With prices softening, you need a bigger margin to attract end buyers. Aim for a 20–30% discount from ARV, not the 10–15% you might have targeted in a hot market.

- Offer creative terms — If the seller is struggling, offer a quick close (30 days) and a clean contract. Sellers value certainty over a higher price.

- Build a buyer's list — In a slower market, end buyers are pickier. Maintain a list of cash buyers, flippers, and landlords who are actively looking for deals. Use a CRM like GoHighLevel to track their preferences.

What Software Tools Help You Manage Wholesaling Contracts?

Managing contracts, leads, and deals manually is a recipe for mistakes. The Wholesale REI directory tracks 63 software tools across 9 categories to help you streamline your wholesaling business. Here are a few that directly relate to contracts:

- GoHighLevel — CRM and marketing automation to manage your leads and follow-ups.

- PropStream — Property data and analytics to find motivated sellers and estimate ARV.

- ATTOM Data — Comprehensive property data for market analysis.

- CallTools — Power dialer for reaching more sellers faster.

- Launch Control — Lead management and campaign tracking.

- Rezzie — All-in-one platform for wholesalers including contract templates.

Using these tools can help you find better deals, communicate with sellers, and close assignments faster.

How to Choose the Right Tools for Your Business

- If you're just starting out — Use a simple CRM like Google Sheets or a free tier of HubSpot. Focus on building your buyer's list and practicing your pitch.

- If you're doing 1–5 deals per month — Invest in PropStream for property data and GoHighLevel for lead management. Use Rezzie for contract templates.

- If you're scaling to 10+ deals per month — Add CallTools for power dialing, ATTOM Data for bulk data analysis, and Launch Control for campaign tracking. Consider hiring a virtual assistant to manage the software.

The Bottom Line

Real estate wholesaling contracts are the backbone of your business. Master the assignment clause, choose between an assignment or double close based on your state's laws, and always give yourself enough time to find a buyer. With the median home price at $403,200 and mortgage rates at 6.49%, wholesaling remains a powerful way to profit in real estate without using your own money. Your next step? Compare the contract management and lead generation tools in our directory to find the right fit for your workflow. And if you want to practice your seller conversations, try our free AI Cold Call Trainer — it's a safe way to sharpen your pitch before you pick up the phone.

Frequently Asked Questions

What is a real estate wholesaling contract?

A real estate wholesaling contract is a purchase agreement between a wholesaler and a seller that includes an assignment clause, allowing the wholesaler to transfer their rights to an end buyer before closing.

What is the difference between an assignment of contract and a double close?

In an assignment, you transfer your contract rights to an end buyer who closes with the seller. In a double close, you actually buy the property (using transactional funding) and then resell it to the end buyer on the same day.

What clauses must a wholesaling contract include?

Key clauses include an assignment clause, inspection period, clear purchase price and terms, no financing contingency (or assignable financing), time is of the essence, and an entire agreement clause.

Is wholesaling real estate legal in all states?

Wholesaling is legal in most states, but some have restrictions. For example, Florida requires a license for certain deals, and Georgia requires a written agreement with the seller. Always check your state laws.

How do I find an end buyer for my wholesale contract?

You can find end buyers through your network, social media, real estate investor groups, or platforms like PropStream. Marketing the contract as a "deal" to other investors is common.

What is an assignment fee in wholesaling?

An assignment fee is the profit you make when you assign your contract to an end buyer. It's the difference between the price you negotiated with the seller and the price the end buyer pays you.

Sources

- Software tools tracked in the Wholesale REI directory — Wholesale REI directory

- Tool categories in the Wholesale REI directory — Wholesale REI directory

- 30-Year Fixed Mortgage Rate (as of 2026-06-25) — FRED (Federal Reserve Bank of St. Louis)

- Median Sales Price of Houses Sold (as of 2026-01-01) — FRED (Federal Reserve Bank of St. Louis)

- Median Days on Market (as of 2026-05-01) — FRED (Federal Reserve Bank of St. Louis)

This article was researched and drafted with AI assistance, then reviewed and edited by Mark Anthony. Every statistic is sourced and cited. It's for informational purposes only and is not financial or legal advice. Read our editorial policy.